Know what buyers will find—before they find it.

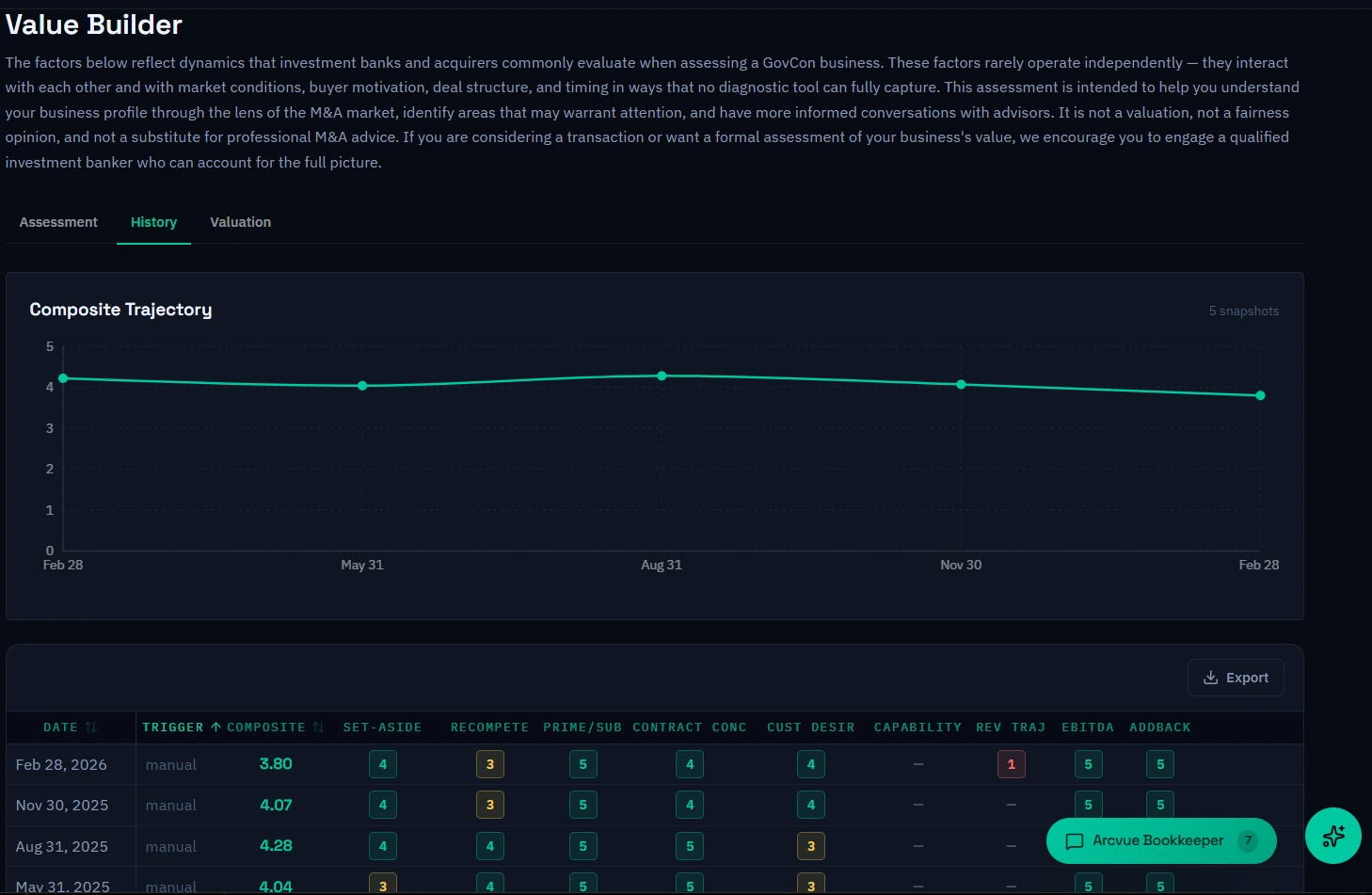

The firms that command the strongest sell-side outcomes are not the ones that optimized for the process. They are the ones that built the right business for years before the process happened. Value Builder tracks 10 key attributes buyers and lenders evaluate—set-aside concentration, contract concentration, prime/sub mix, recompete risk, customer desirability, capability profile, revenue trajectory, EBITDA margin, addback quality, and management depth—continuously against your live ERP data.

Every close, the assessment updates. The History tab shows how your profile has moved over time. If a banker or lender has given you feedback on specific attributes, set a goal and the platform tracks it automatically—no manual check-ins, no spreadsheet. A CEO who has been running Value Builder for two years walks into a banker meeting already knowing what the banker is going to say. That is a different conversation.