Is this deal financeable? Know today, not in two weeks.

When a target comes across your desk, the first question isn't the multiple—it's what the combined entity looks like and whether you can finance it. That answer normally takes two weeks of banker modeling against projections built from the ground up. Arcvue has your operating baseline already. The deal terms are the only new inputs.

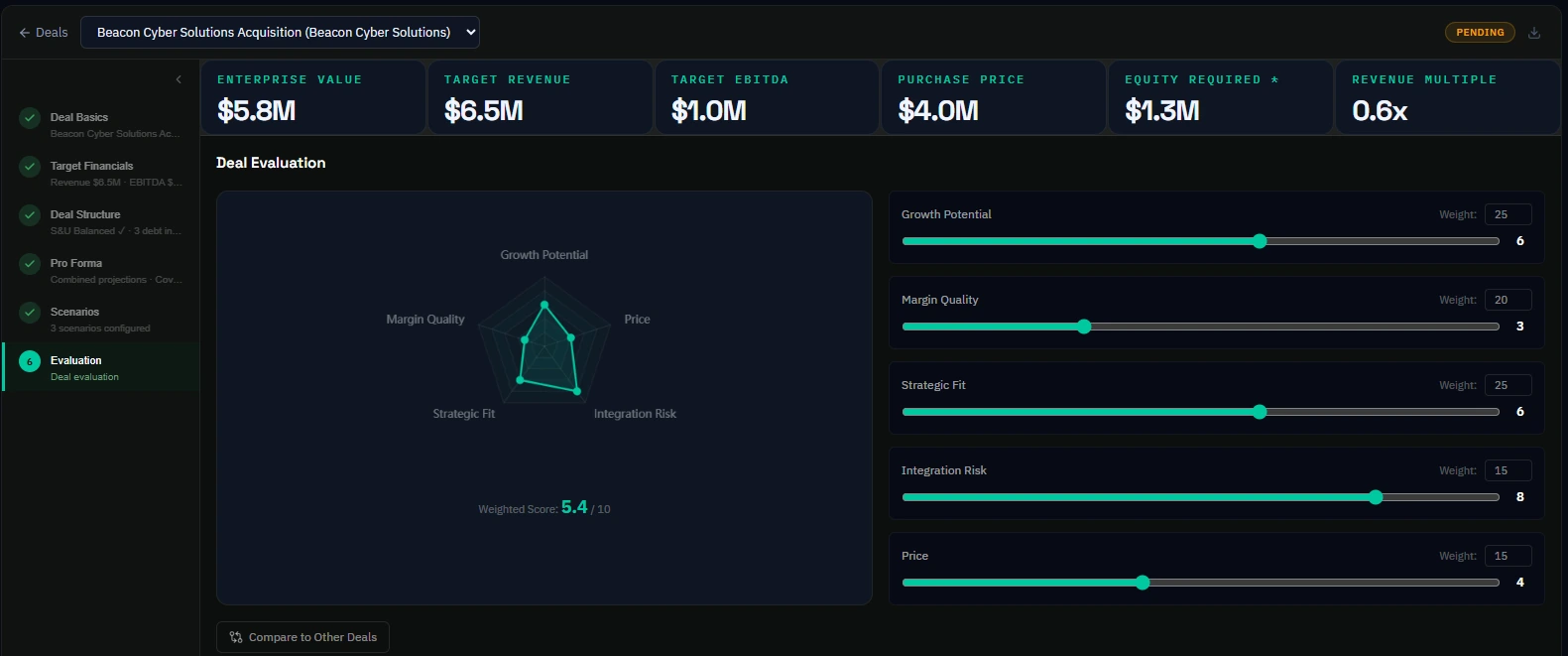

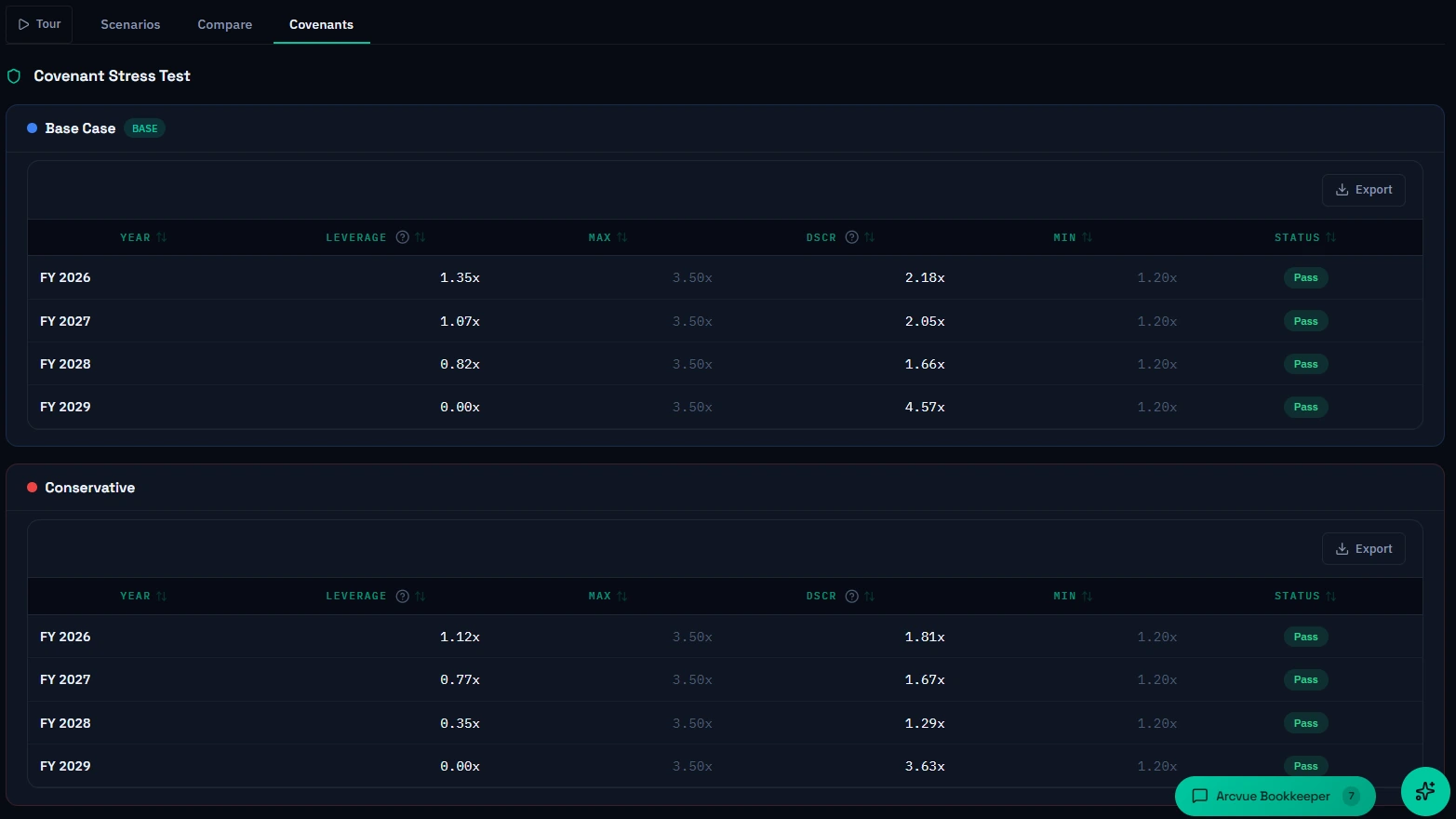

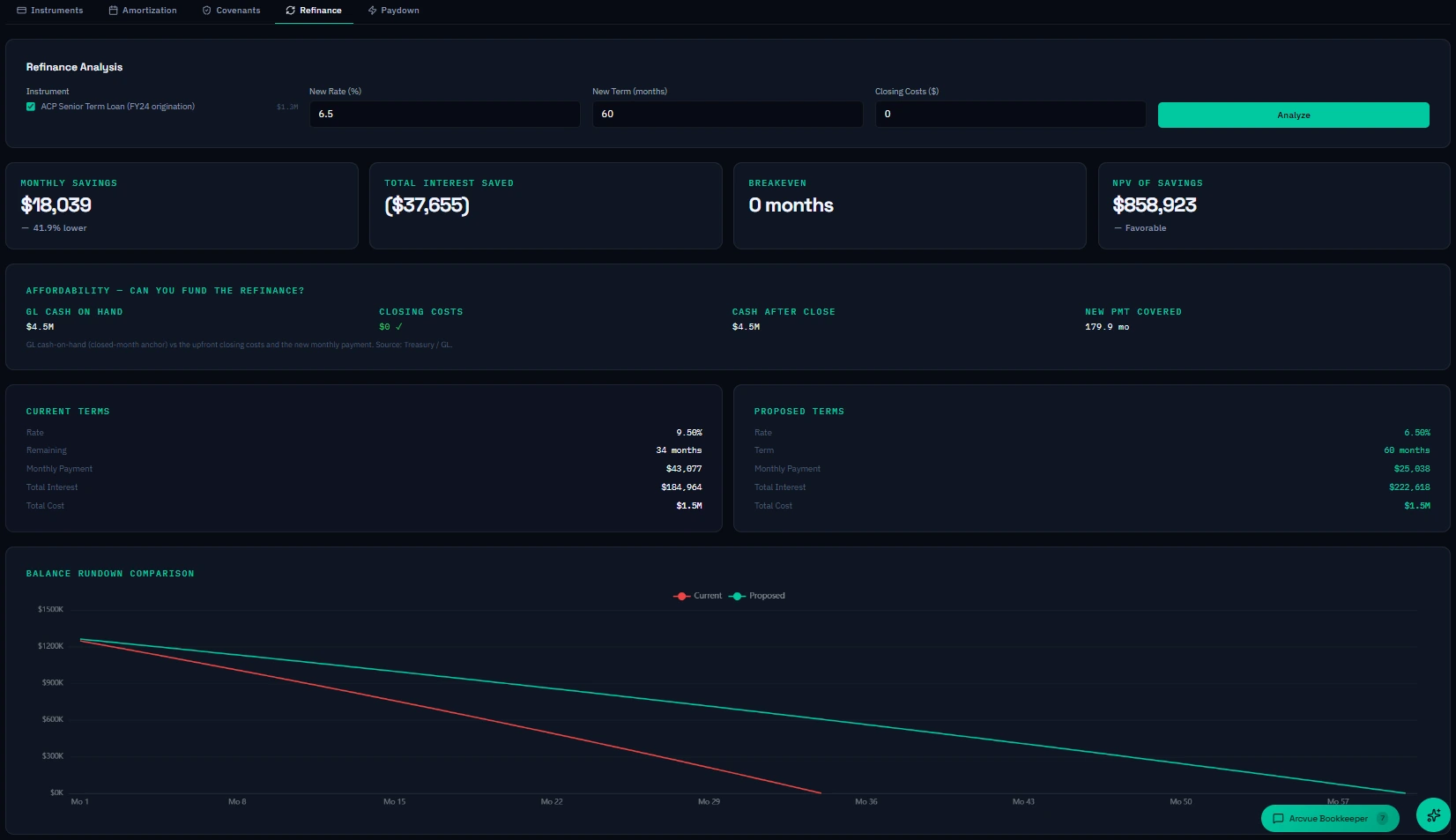

Enter the target's revenue, EBITDA, and purchase price. Select a debt structure—traditional senior, unitranche, or seller-financed. Arcvue computes sources and uses, post-close three-statement projections, covenant compliance under the combined debt load, and equity return at exit—all against your actual P&L and balance sheet from last night's ERP sync. The combined entity's indirect rate structure reflects both companies' actual cost pools. The covenant projections use your real debt schedule and your actual credit agreement thresholds, not placeholders.

Multiple deals can be evaluated simultaneously. A two-target acquisition—evaluating two tuck-ins at once and modeling the combined entity against your platform company—runs in the same workspace. Each target has its own financials. The combined sources and uses, debt structure, and covenant compliance reflect all three entities together. The analysis that previously required a separate model for each permutation runs in one place, against the same baseline, with results that are directly comparable.

Post-close integration is handled through multi-entity consolidation. Both ERPs connect to Arcvue independently on day one of the hold. The combined P&L, indirect rate structure, and covenant metrics are available the morning after onboarding—not six months into an ERP integration project that may never fully resolve. For PE-backed platforms evaluating add-ons, this means the combined view exists before the ink is dry.

- Deal analysis against your live ERP data—actual P&L, actual indirect rates, actual debt schedule—not a model built from scratch

- Full three-statement post-close projections—P&L, cash flow, and balance sheet all respond to the same deal terms

- Multi-target evaluation—model one, two, or three simultaneous acquisitions against your platform company baseline

- Sources and uses, debt structure selection, and equity return at exit computed automatically

- Covenant compliance tested against your actual credit agreement thresholds—not generic benchmarks

- Post-close multi-entity view available day one through independent ERP connections—no integration project required