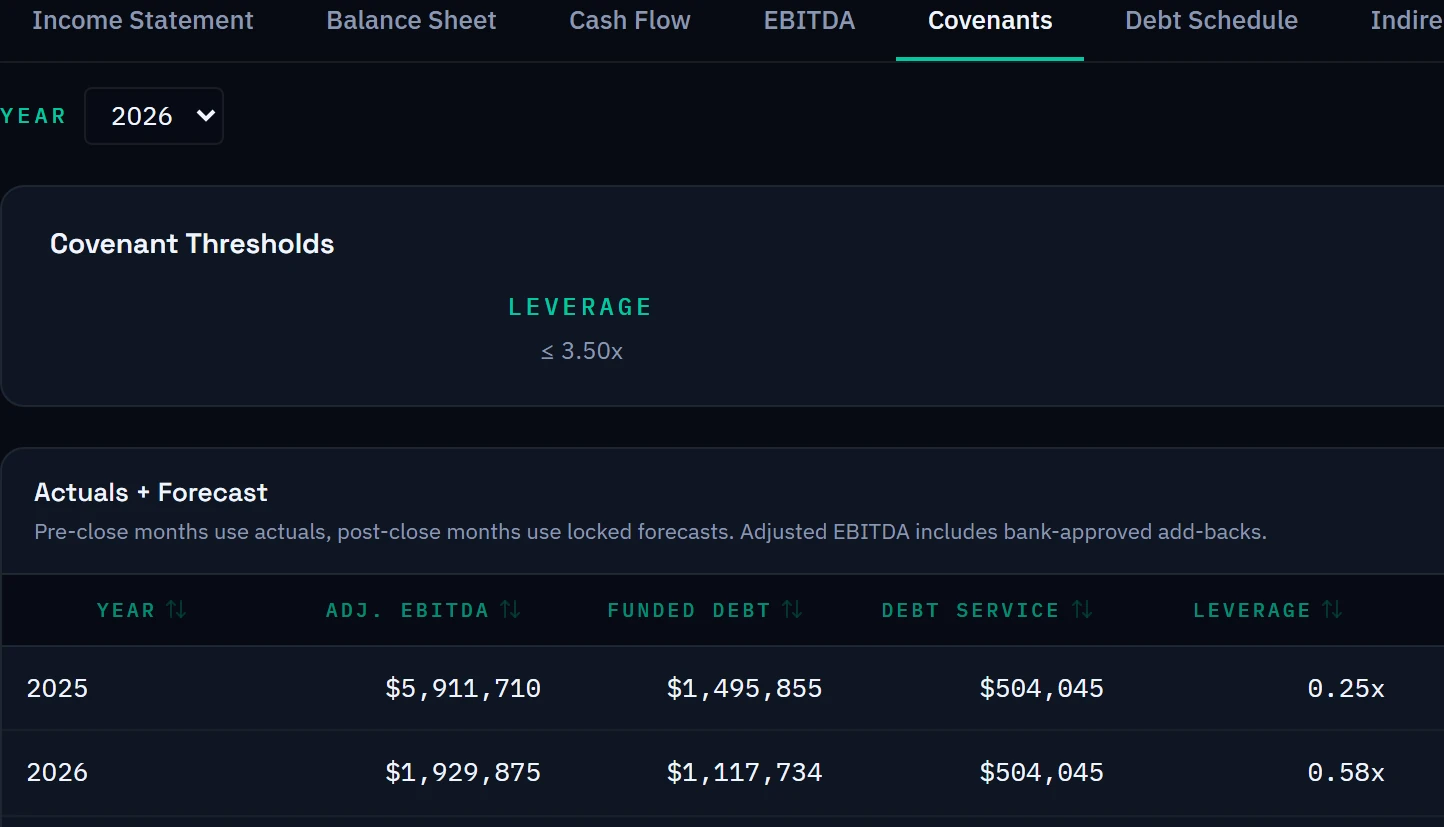

Covenant compliance computed nightly—not assembled quarterly.

When your borrower is on Arcvue, DSCR and leverage are computed nightly from actual ERP data—not from a model the controller builds when the quarterly certificate is due. The EBITDA figure uses your bank-approved add-backs: owner compensation normalization, one-time transaction costs, D&A, and any other items your credit agreement specifies. The leverage calculation excludes revolver principal if your covenant definition requires it. The numbers follow your definitions, not the borrower's approximation of them.

Configurable lender access lets you see exactly what you've agreed to see—P&L, cash position, forward covenant projections, debt schedule—updated nightly from the ERP. When a ratio is drifting, you see it as it develops. When it's healthy, you know that too—with numbers you can show your credit committee, not with assurances from a management call. The quarterly covenant certificate becomes a confirmation of what you've already been monitoring, not a report you're trusting on faith.

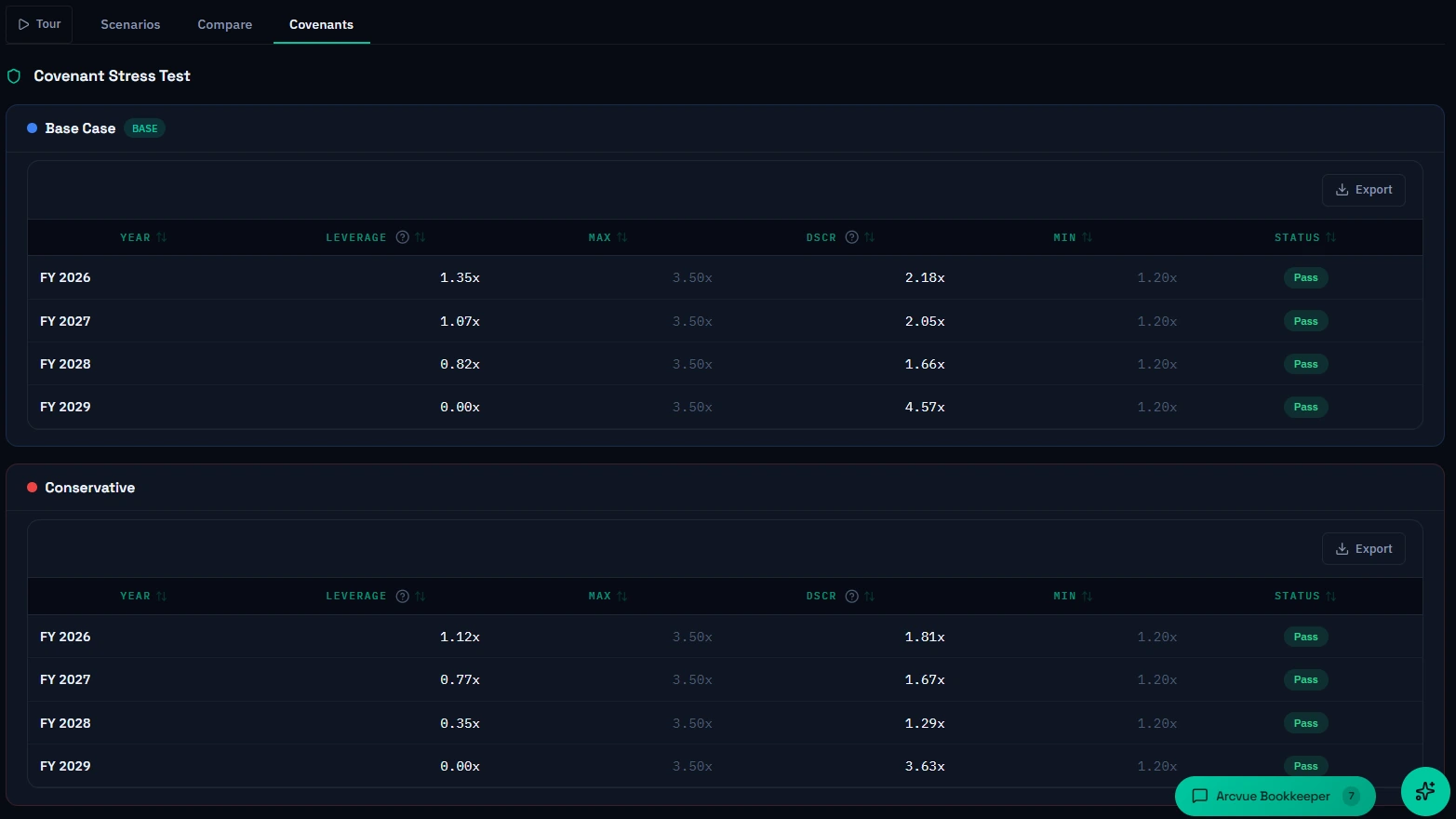

Three forward scenarios—base, upside, and downside—project covenant compliance six months out using the current operating forecast and actual debt schedule. When a contract the borrower is pursuing matters to their covenant compliance, you see the scenario analysis before the award is made. The relationship moves from reactive to collaborative—not because the borrower changed, but because you both have the same information at the same time.