From CIM to financeable deal analysis—the same afternoon.

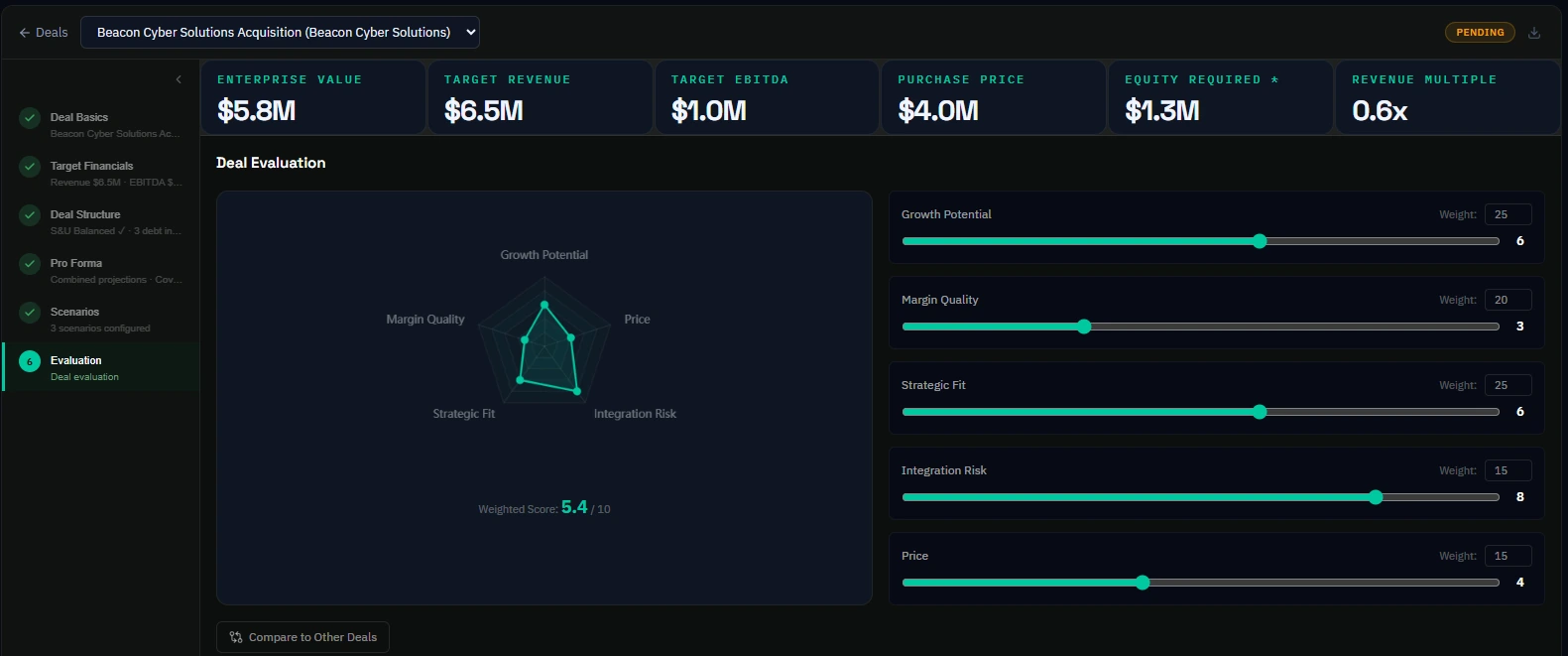

Arcvue has your actual operating baseline—last night's P&L, this morning's indirect rates, your current debt schedule and covenant thresholds. Enter the target's revenue, EBITDA, and purchase price. Select a debt structure. The platform computes sources and uses, post-close three-statement projections, covenant compliance under the combined debt load, and equity return at exit—all against your real numbers, not a generic model built from scratch for this deal.

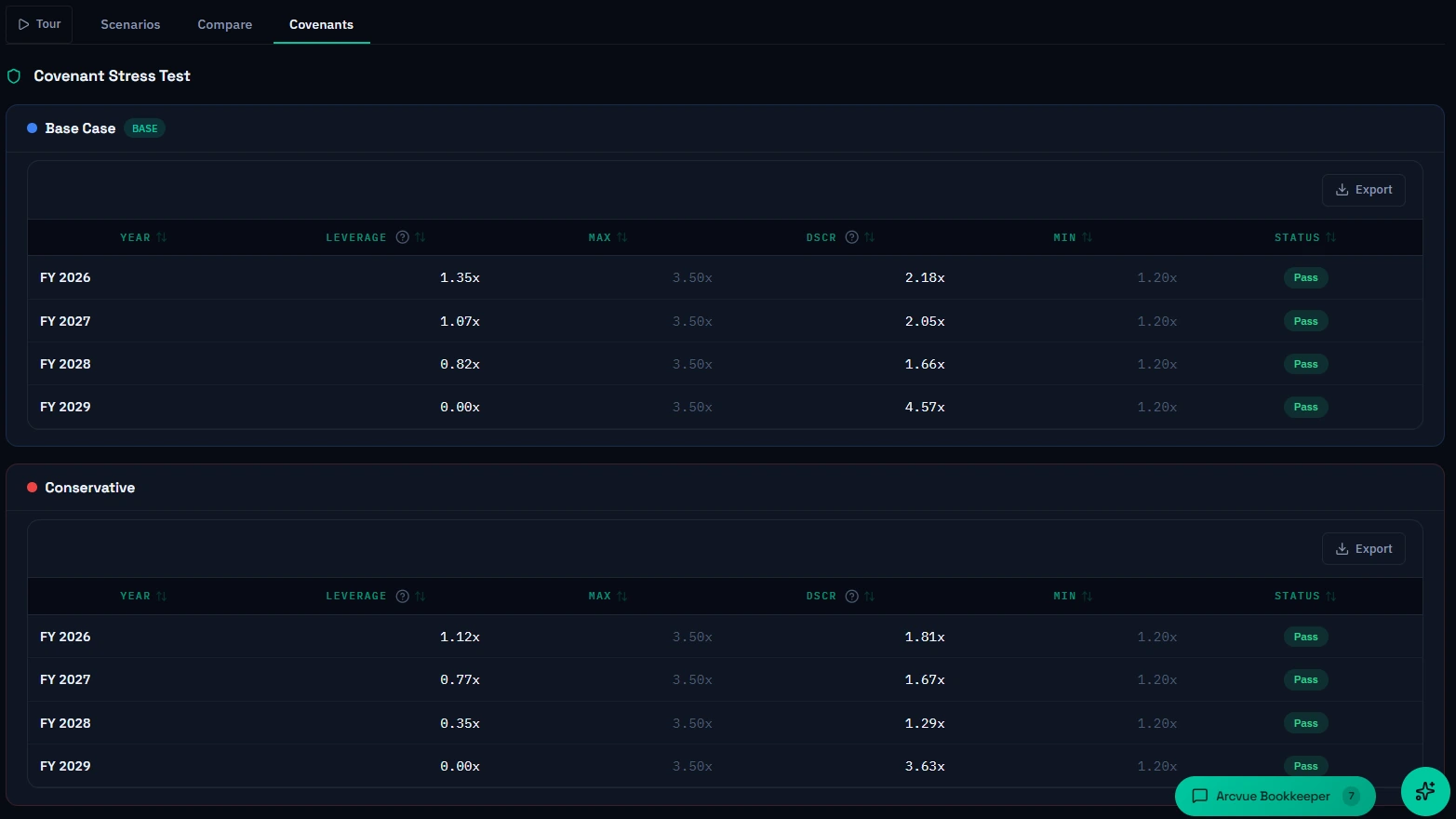

The combined entity's indirect rate structure reflects both companies' actual cost pools. The covenant projections use your real debt schedule and your actual credit agreement thresholds—not benchmarks. The post-close cash flow projection accounts for your actual debt service, your actual LOC behavior, and the target's actual burn rate. The analysis you get isn't an approximation. It's your real financial position with the deal terms layered on top.

When the seller asks where you are, you have an answer. When your banker asks if the deal is financeable, you know before the conversation starts. The two weeks of preparation time collapses into an afternoon because the preparation was done the day you connected your ERP—not the day the deal arrived.